To begin with, the global financial landscape is currently experiencing a profound MacroUpdate as Wall Street braces for the critical data dump scheduled for this Thursday. Specifically, investors are intensely focused on the upcoming 4th quarter GDP revision and the weekly jobless claims report. Consequently, this anticipation has introduced a fresh wave of strategic rebalancing into the MacroUpdate for this trading session. Institutional players are now meticulously scanning for alpha in a market that remains sensitive to any hint of economic cooling. You can monitor the real-time impact on market indices and bond yields through Yahoo Finance (https://finance.yahoo.com).

1. The Ominous GDP Revision and MacroUpdate Analysis

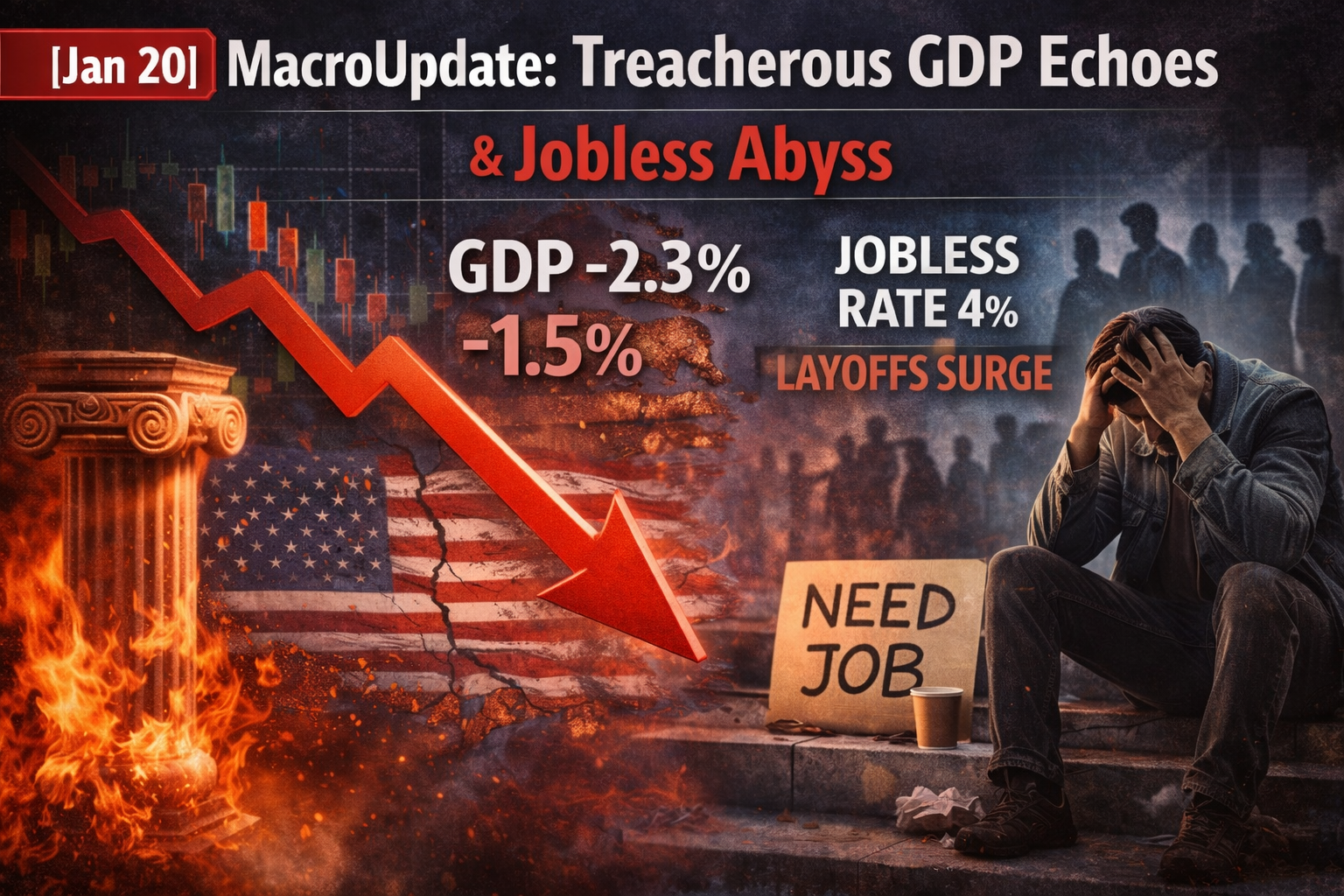

First, the financial world is bracing for the 4th quarter GDP final estimate as current MacroUpdate signals indicate a heightened state of alert. While previous readings suggested resilience, any downward revision could reignite fears of a looming stagflationary environment. In addition, this MacroUpdate shift has triggered a selective rotation out of cyclical sectors and into those with proven pricing power. According to Investing.com (https://www.investing.com), the consensus expectation remains centered around a steady growth rate, but whispers of a miss are growing.

Furthermore, various Fed officials have recently emphasized that policy decisions will remain data-dependent regardless of historical growth markers. Therefore, the optimistic “soft landing” narrative is currently being stress-tested by a reality of persistent service-sector inflation. This pivot in monetary expectations is a core component of today’s MacroUpdate, as market participants adjust their terminal rate projections. Moving forward, the focus remains on whether the revised growth figures can justify the current equity valuations.

2. MacroUpdate: The Jobless Claims Shock & Labor Friction

In addition, the weekly initial jobless claims report due this Thursday has become a pivotal point in the MacroUpdate. Because the labor market has been the primary shield against recession, any spike in claims could trigger a massive sell-off. Consequently, the MacroUpdate regarding global industrial stability has turned somewhat cautious as major tech firms continue their quiet headcount reductions. Reuters (https://www.reuters.com) reports that layoff announcements have reached levels not seen since the peak of the previous cycle.

Moreover, the higher cost of labor acts as a direct headwind for small-cap companies and domestic manufacturers today. Since margin preservation is a key driver of quarterly performance, this move is being watched closely by macro strategists. The MacroUpdate suggests that regions with diversified employment bases will likely outperform their single-industry counterparts in the near term. In conclusion, the jobless data remains a dormant volcano that could disrupt the market’s recovery path if numbers exceed expectations.

3. The Yield Curve Paradox and MacroUpdate

On the other hand, a broad divergence is taking place within the bond market as a fresh MacroUpdate favors short-term liquidity. Therefore, the 10-year Treasury yield is seeing high-conviction moves that suggest a deep skepticism regarding long-term price stability. This trend connectivity is a critical component of our current MacroUpdate, as investors move beyond speculative growth into tangible safety. The Wall Street Journal (https://www.wsj.com) notes that capital expenditure in defensive assets is expected to reach record highs this quarter.

Furthermore, the regulatory cloud over global financial institutions is darkening as new capital requirement rules are debated. Since these entities rely heavily on stable interest rate environments, any significant legislative change could impact their lending trajectories. The MacroUpdate for the banking sector is now one of heightened scrutiny and strategic diversification by major fund holders. In addition, smaller regional banks are struggling to maintain momentum as capital flows move toward the safety of the too-big-to-fail.

4. Institutional Sentiment: JP Morgan’s MacroUpdate Warning

In addition, JP Morgan’s strategy team issued a note this morning regarding the “unprecedented” valuation gap in the current MacroUpdate. Since a handful of sectors are driving the majority of index gains, the bank warns of potential fragility. Furthermore, the report suggests that a broadening of the market rally is necessary to sustain the current upward momentum. Bloomberg (https://www.bloomberg.com) reports that institutional positioning in defensive sectors has reached a two-year high recently.

Moreover, the report highlights the risk of a “liquidity void” if the upcoming GDP data misses the mark significantly. Consequently, investors are being advised to look for opportunities in the high-yield cash space where risks are more contained. The MacroUpdate is clear: while the headline indices look strong, the underlying breadth remains a significant concern for investment professionals. Therefore, the bank is recommending a balanced approach, blending cash equivalents with high-quality defensive names for the week.

5. MacroUpdate: The Retail Capitulation Signal

Finally, data from retail trading platforms shows a surge in defensive put buying, indicating a growing anxiety within the MacroUpdate. However, many contrarian analysts believe this excessive fear could be a signal for a short-term tactical bounce. Moving forward, the MacroUpdate will depend on whether these retail-driven hedges can withstand a potential post-GDP volatility spike. More detailed analysis and real-time market selections can be found at DailyStockPicksAI (https://dailystockpicksai.com/).

Investor Outlook

In summary, the current MacroUpdate is defined by a delicate balance between growth optimism and labor market caution. Moving forward, investors should prioritize liquidity and focus on industries with genuine structural moats and sustainable margins. The era of “easy money” has passed, and the market is now rewarding fundamental strength over speculative potential. Navigating this MacroUpdate requires a disciplined eye, favoring high-quality earnings and robust cash flow generation. Expect continued sector rotation as the market digests the next wave of economic data and central bank signals.